Some of our associates are permabears. They are intelligent monetary consultants and planners that usually are usually bearish. We purpose to them for a whole analysis of what can fail for the financial local weather and the inventory trade. They are actually singing and fuel nice offers of pessimism relating to the long run amongst the financial press and most of the people.

In motion, to supply some equilibrium, we analyze what can go proper. Often, we find that the permabears have really missed out on one thing of their evaluations. Since they emphasize the downsides, they regularly cease working to see the positives, or they place unfavorable rotates on what’s mainly favorable.

We seldom have something to contribute to the bearish state of affairs because the bears’ evaluations typically are usually so thorough. So our efforts to supply equilibrium regularly create us to emphasise the positives whereas nonetheless recognizing the downsides. Not remarkably, we get hold of slammed for being as nicely favorable when it pertains to the overview for the United States financial local weather and inventory trade and acquire referred to as “permabulls.”

That’s alright with us, contemplating that the United States financial local weather regularly expands at a powerful fee, and the inventory trade has really gotten on a good lasting uptrend consequently. Consider the next:

1. Recessions are irregular and don’t final lengthy

In the United States, the National Bureau of Economic Research (NBER) is the authority that specifies the start and ending days of financial downturns. According to the NBER, the atypical United States financial downturn over the length from 1854 to 2020 lasted round 17 months.

In the article-World War II length, from 1945 to 2023, the atypical financial downturn lasted round 10 months. Since 1945, there have really been 12 financial downturns that occurred all through merely 13% of that point interval.

2. Bear markets are moreover irregular and don’t final lengthy contemplating that they typically are usually introduced on by financial downturns

There have really been 28 bearishness within the S&P 500 contemplating that 1928, with a typical lower of 35.6%. The atypical measurement of time was 289 days, or roughly 9.5 months. ABC News reported that contemplating that World War II, bearishness usually have really taken 13 months to go from prime to trough and 27 months for the availability fee index to get well shed floor. The S&P 500 index has really dropped roughly 33% all through bearishness over that point framework.

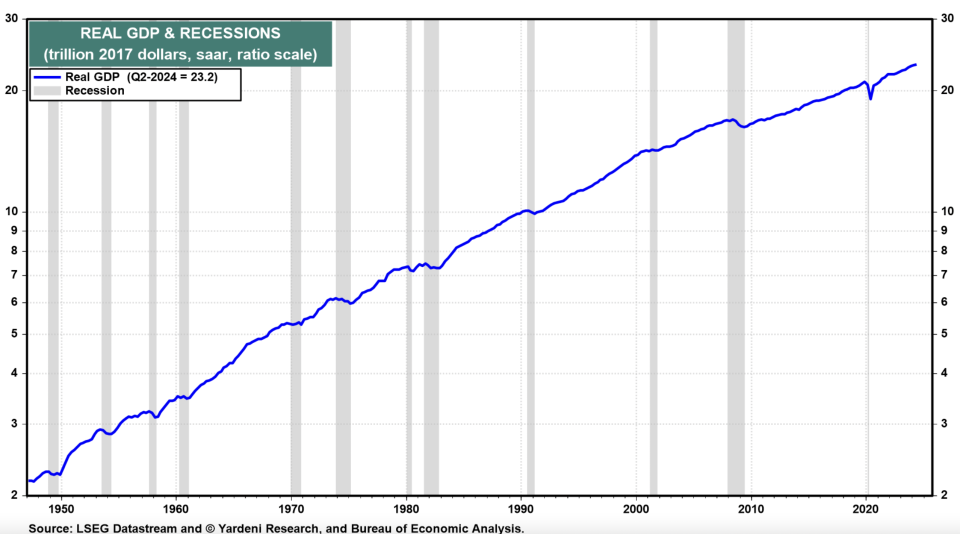

3. United States Economy: Significant Upward Revisions Show No Landing

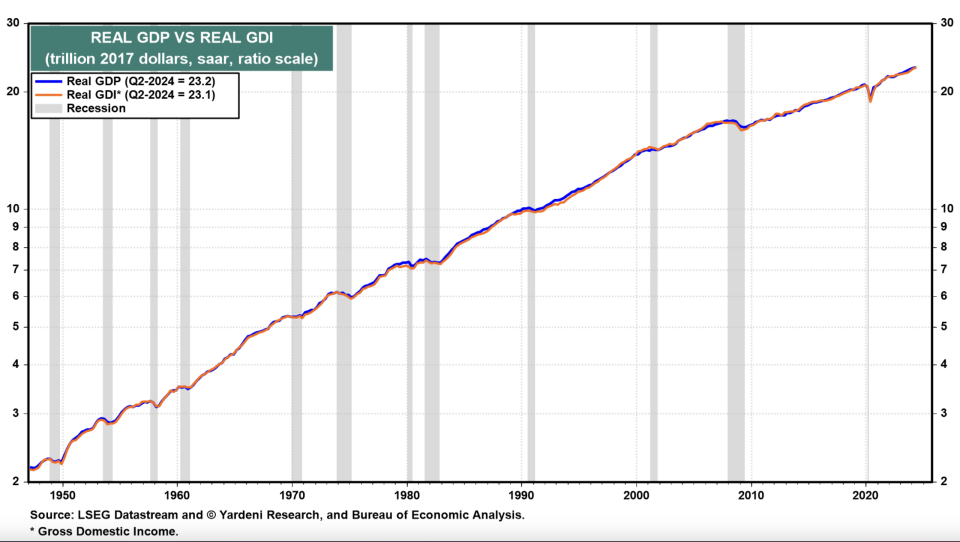

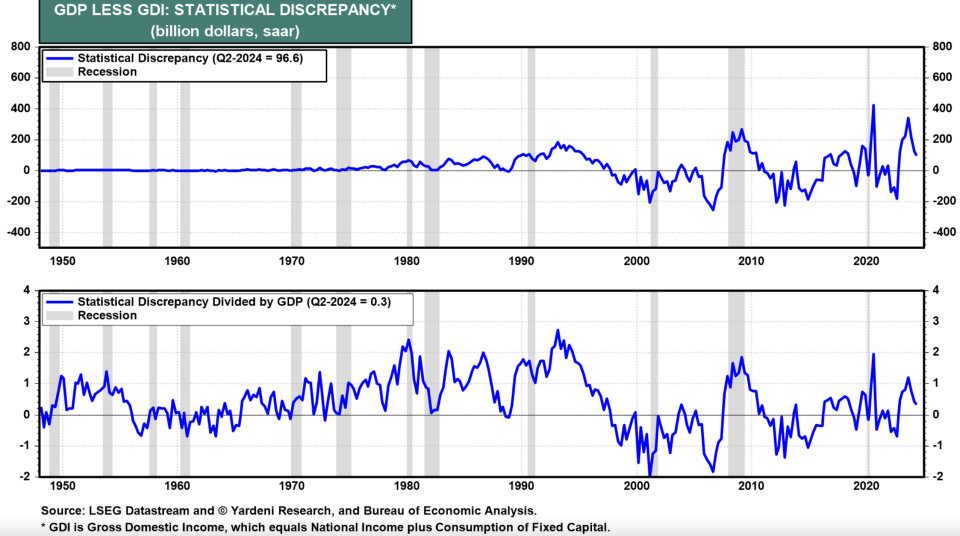

Among the present cynical circumstances of the permabears is that precise Gross Domestic Production (GDP) has really been increasing faster than precise Gross Domestic Income (GDI). The 2 alternate actions of the United States financial local weather have considerably diverged, recommending that one thing is wrong with the precise GDP data which it’s sure to be modified downward, fixed with the cynics’ pessimism. They haven’t mentioned why they think about the GDI data to be a way more precise step of economic job than the GDP data.

Indeed, the Bureau of Economic Analysis (BEA), which places collectively each assortment, prefers GDP over GDI: “GDI is an alternative way of measuring the nation’s economy, by counting the incomes earned and costs incurred in production. In theory, GDI should equal gross domestic product, but the different source data yield different results. The difference between the two measures is known as the ‘statistical discrepancy.’ BEA considers GDP more reliable because it’s based on timelier, more expansive data.”

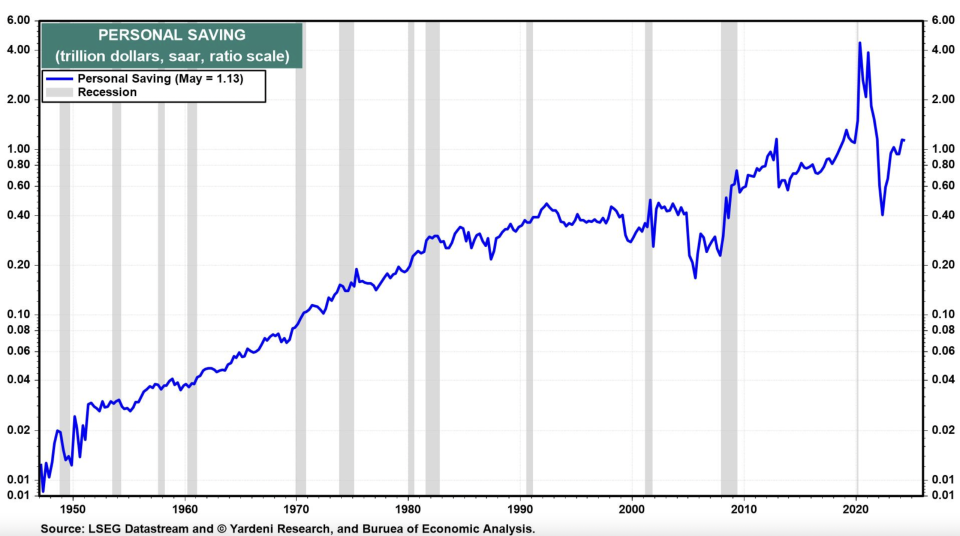

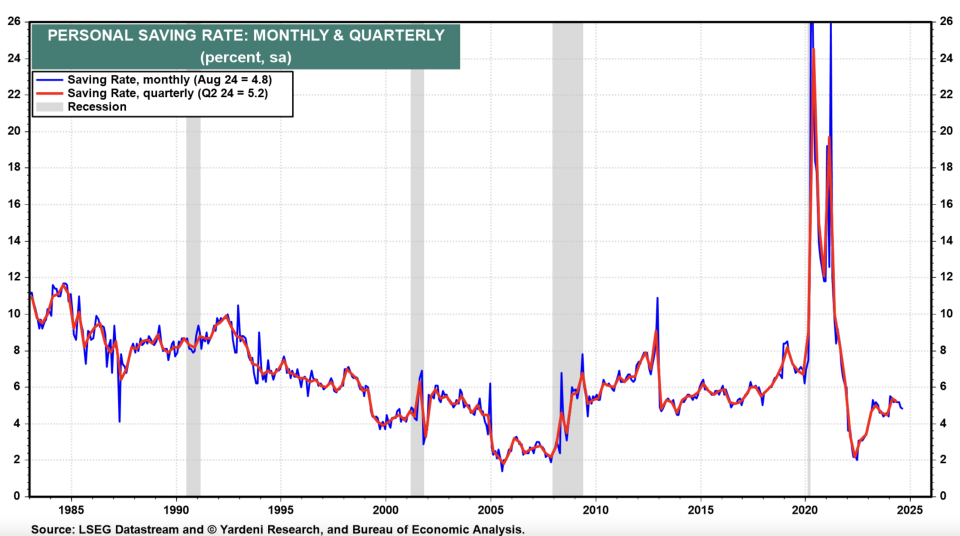

Meanwhile, the permabears have really moreover been calling the alarm system bell relating to the person conserving value lately. It had really gone down to three.3% all through Q2-2024, based on the earlier value quote, essentially the most reasonably priced contemplating that Q3-2022. One permabear composed on September 25 that “historical past suggests when the SR sinks this low, it often proves unsustainable with a subsequent rise triggering a recession.

The slide within the SR from 4% at first of this yr was not as a consequence of households dipping into to their pandemic-era extra financial savings, which have been lengthy since spent. But it appears that evidently households have grow to be used to working down their financial savings and may’t break the behavior.” His verdict was that “the super-low US saving ratio [is] a ticking economic timebomb.”

The actually following day, on September 26, the BEA launched its latest modifications of Q2-2024 GDP and GDI. Much to the disgrace of the permabears, precise GDI was modified considerably better, led by the next modification in earnings and wages– which moreover created a considerable increased modification within the particular person conserving value!

Here is the delighted data from the BEA:

( 1) GDP & & GDI.

Real GDI enhanced 3.4% (saar) in Q2, the next modification of two.1 ppts from the earlier value quote.Real GDP climbed an unrevised 3.0% all through Q2. The normal of precise GDP and precise GDI– a supplementary step individuals monetary job that simply as weights GDP and GDI– enhanced 3.2% in Q2, the next modification of 1.1 ppts from the earlier value quote.

Even Q1’s numbers had been modified better, additionally a lot to the bears’ disgrace. Real GDP was modified up from 1.4% to 1.6%, and precise GDI was modified up from 1.3% to three.0%. The normal of the GDP and GDI was elevated from 1.4% to 2.3%.

The analytical disparity in between each actions of the financial local weather is small presently. In present bucks, it was modified to 0.3% from 2.7% all through Q2.

( 2) Personal value financial savings

Personal conserving was $1.13 trillion in Q2, the next modification of $74.3 billion from the earlier value quote.

The particular person conserving value– particular person conserving as a % of non reusable particular person earnings– was 5.2% in Q2, in comparison with 5.4% (modified) in Q1. The earlier quotes for the conserving value had been 3.3% in Q2 and three.7% in Q1.

( 3) Wages & & wages(* )upwards modifications to each the GDI and the person conserving value confirmed the next modification in small earnings and wages settlement.

The buyer investing was strong all through the very first fifty % of the yr, whereas the person conserving value stayed pretty excessive, and undoubtedly greater than the So projection.“timebomb”( 4)

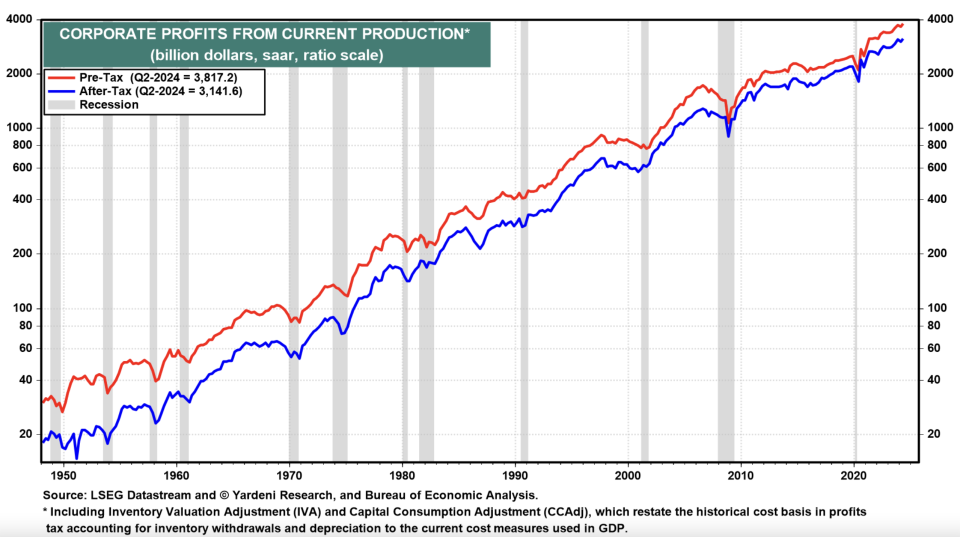

earningsCorporate’s far more:

There- tax obligation enterprise profit from present manufacturing (enterprise earnings with provide analysis and funding consumption modifications) was modified up by 3.5% to a doc $3.1 trillion (saar).After/

So growing to a brand-new doc excessive of $2.0 trillion was enterprise returns.

Also( 5)

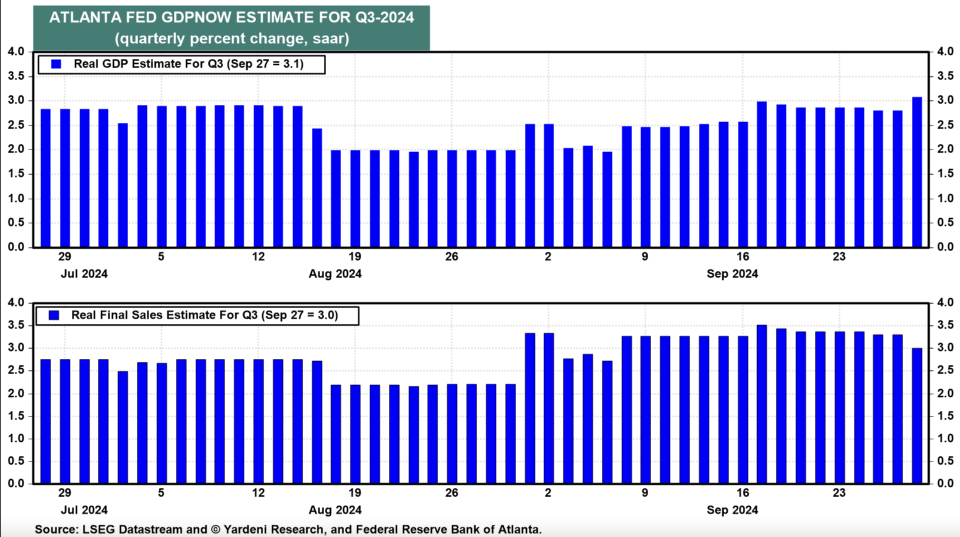

Q3’s GDP. present quarter will definitely stay to annoy any sort of staying hard-landers.

The’s The Atlanta Fed model reveals precise GDP up 3.1% (saar) all through Q3. GDPNow‘s the next modification from 2.9% on That 18.September GDP

Real( 6)

landing. No latest BEA modifications additionally removed the technological financial downturn all through H1-2022 when precise GDP dropped 2.0% and 0.6% all through Q1 and Q2 of that yr.

The 2 numbers had been modified to -1.0% and 0.3%.Those proceeds to not seem.

The “Godot recession”, a transferring financial downturn has really struck a few markets that had been most acutely aware the tightening up of economic plan. Instead the final financial local weather has really stayed sturdy and far much less interest-rate delicate than up to now.But an final result of the newest standards modifications, Q2’s precise GDP and precise GDI are 1.3% and three.8% increased than previously approximated.

As’s no robust or mushy landing within the modifications. There financial local weather continues to be flying excessive, because it has really been contemplating that the two-month pandemic financial downturn all through The and March 2020!April,

So the Why Did? Fed Ease’s an excellent inquiry supplied all of the above.

That answer is that

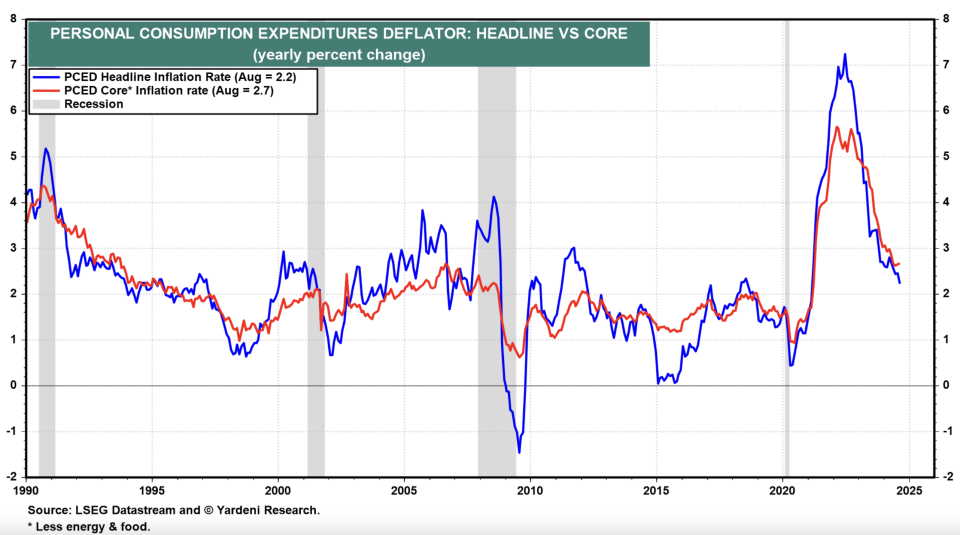

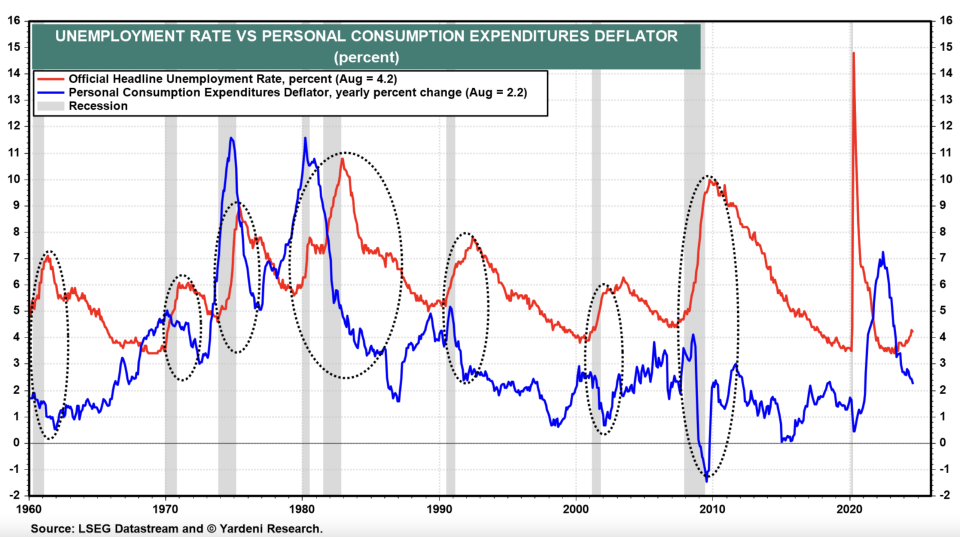

The knowledgeable the Congress to scale back by mandating that monetary plan must intend to keep up each the rising value of dwelling and the joblessness costs lowered. Fed authorities can undoubtedly declare that they’ve really achieved this wonderful harmonizing act. Fed, the joblessness value was simply 4.2%, and heading and core PCED rising value of dwelling costs had been to 2.2% and a couple of.7%.In August PCE

Fed it was achieved with out an financial downturn as was wanted up to now to do the duty.“Mission accomplished!” And PCED

However andApril January’s the main issue that That & &Powell decided to scale back the federal government funds value by 50bps lately.Co picked to miss

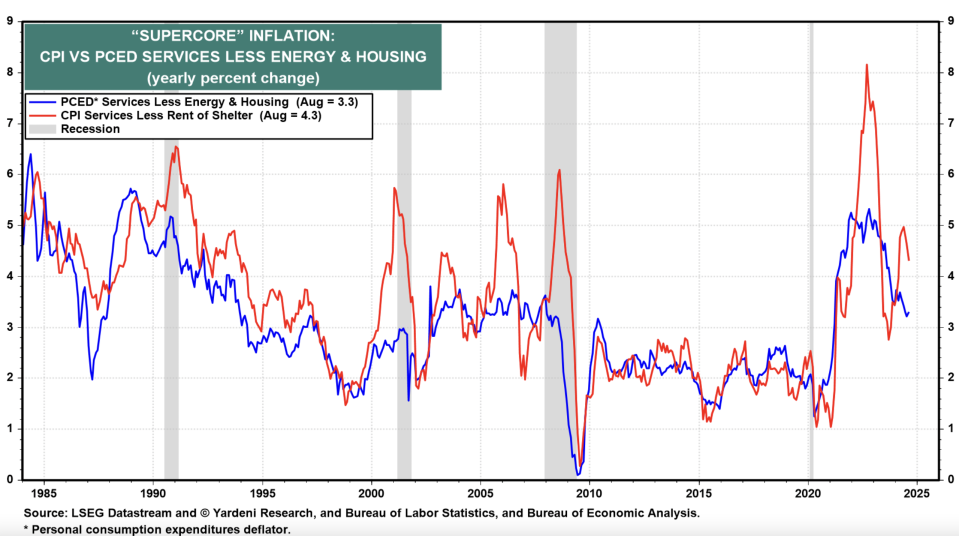

They’s sticky analyses of the August rising value of dwelling value (i.e., buyer fee rising value of dwelling for options leaving out energy and actual property), which was 3.3% for the PCED and 4.3% for the CPI.“supercore” their objective isn’t completely achieved thought-about that

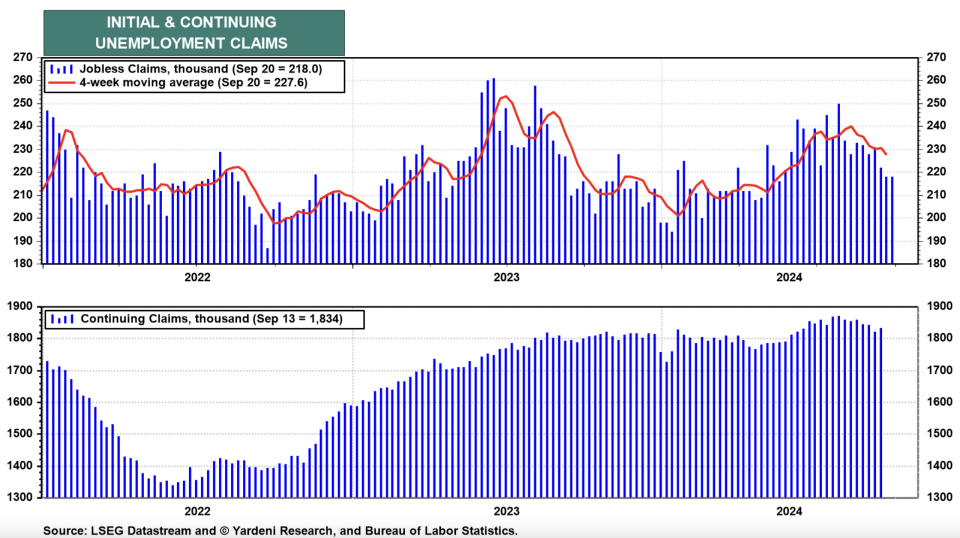

So very first mentioned Fed Chair Jerome Powell rising value of dwelling in his speech on the “supercore” on Hutchins Center and Fiscal on the Monetary Policy again on Brookings Institution 30, 2022. November made a big provide relating to it. He noticed that it made up over half of the core PCE index. He no extra discusses it.He, discharges proceed to be restrained, as proven by the most recent preliminary joblessness asserts data.

Meanwhile & &

Fed their easing of economic plan is targeted on growing monetary want and the necessity for labor, i.e., job openings, which stayed over the pre-pandemic levels in

So.July/

That can heat up rising value of dwelling. That can the financial plans of the next resident of the So.White House why did the

So authorities select to scale back? Fed why may they continue to be to scale back?And need to accomplish that to forestall an financial downturn and to develop much more job openings.

They need to take the possibility of blowing up buyer prices together with possession prices. They need them good luck. We any sort of event, any sort of staying diehard hard-landers want to remember the previous expression: In.